Global smartphone CMOS Image Sensor (CIS) shipments rose by 2% year-on-year (YoY) to 4.4 billion units in 2024 driven by a recovery in end-market demand, according to Counterpoint Technology Market Research’s Smartphone Camera Tracker. However, the average number of cameras per smartphone further declined to 3.7 units in 2024 from 3.8 units in 2023, despite the market’s recovery.

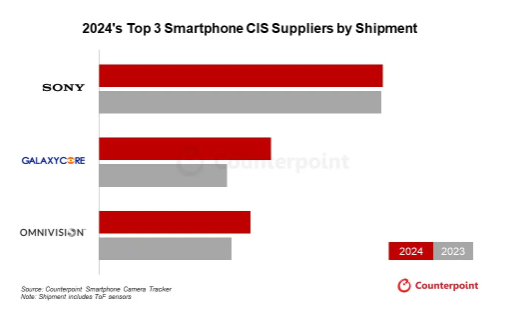

Sony maintained its leading position in 2024, growing slightly YoY, mainly due to improved production yields and increased demand for premium smartphones. Shanghai-based GalaxyCore ranked second with a 34% YoY increase in shipments. Leveraging its cost-effective advantage, the company has captured more Android orders. Additionally, by shifting to a Fab-lite operational model, GalaxyCore has significantly enhanced product competitiveness, accelerating the launch of high-resolution sensors such as 50MP and further refining its product portfolio.

OmniVision’s shipments rose 14% YoY in 2024 driven in part by its expansion in the popular 50MP sensor segment. Offering excellent performance at a more competitive price than rival solutions, its products such as the OV50H image sensor have gained significant traction after launch and have been widely adopted by major Chinese OEMs. Meanwhile, SK Hynix plans to exit the CIS market in 2025 due to intensifying competition. Its withdrawal could open up new growth opportunities for Chinese suppliers including GalaxyCore and OmniVision.

Looking ahead, technological advancements like LOFIC and multispectral, along with OEMs’ ongoing efforts to enhance camera performance, are expected to lift market ASP. However, we expect CIS shipments to see a slight YoY decline in 2025 due to challenges in the global smartphone market stemming from geopolitical tensions and macroeconomic uncertainties. The ongoing reduction in cameras per smartphone also continues to dampen CIS demand.